IATA (International Air Transport Association) has released its data on global air cargo transport for March 2026, reporting a 4.8% year-on-year contraction in demand, measured in cargo tonne-kilometres. For international operations alone, the decline rises to 5.5%. Capacity, measured in available cargo tonne-kilometres, fell by 4.7% globally and by 6.8% on international flights. At the centre of this downturn is the continuing crisis in the Middle East, which has effectively paralysed some of the world’s main cargo handling hubs, disrupting global flows and forcing airlines to reconfigure their operating networks.

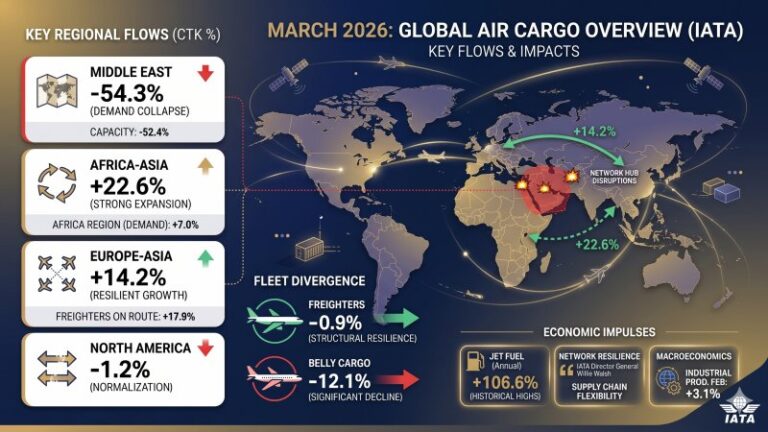

The sharpest regional figure concerns Middle Eastern carriers, which recorded a 54.3% collapse in demand and a 52.4% reduction in capacity. This was the steepest contraction among all regions analysed and reflects the near-total interruption of operations at airports across the region. The most affected routes were those crossing the Gulf corridors: the Middle East-Asia lane fell by 58.6%, while Europe-Middle East declined by 57.6%. Middle Eastern carriers removed 1.742 million units of traffic from the market, a volume that weighed on the entire global air logistics system. Airlines responded to the crisis by reorganising their routes, bypassing closed or restricted airspace and accepting longer, and therefore more expensive, journeys. This redrawing of trade lanes has had knock-on effects across several regions, causing congestion on secondary routes and creating opportunities for carriers operating in areas not directly affected by the conflict.

Asia-Pacific partly benefited from this traffic diversion effect, with demand rising by 5.4% and capacity increasing by 5%. Africa recorded the strongest performance of all regions, with demand up 7%, although capacity fell by 4.6%, signalling operational pressure already affecting the continent’s carriers. The Africa-Asia route rose by 22.6%, marking nine consecutive months of expansion and becoming one of the most dynamic corridors in the entire system.

Europe recorded a 2.2% increase in demand and a 4.2% rise in capacity, with the Europe-Asia lane up 14.2%, an expansion that has now lasted for 37 consecutive months. Growth was driven to a significant extent by dedicated cargo flights, which rose by 17.9% on this route. North America remained broadly stable, with demand down 1.2% and capacity falling by 1.1%, a trend that IATA links to the normalisation of volumes after the peak recorded in 2025, when imports were brought forward in response to tariff tensions.

March 2026 showed a clear divergence between the performance of dedicated freighter aircraft and passenger flights using bellyhold capacity for cargo. Demand carried in the bellyhold fell by 12.1%, hit by dependence on rigid schedules and on hubs that suffered severe disruption in the Middle East. Dedicated freighters, by contrast, showed considerable resilience, with a global decline of just 0.9%, confirming their role as a more flexible and reliable tool during crises, particularly in maintaining supply chain continuity on Asian routes.

The trend in jet fuel costs is adding further pressure on the sector. According to IATA data, the price rose by 106.6% year on year in March, reaching its highest level in 23 years, alongside a 43.1% increase in Brent crude and a 320% surge in refining margins. Longer routes imposed by diversions around crisis zones further amplify the impact of this energy shock, as higher fuel consumption is added to an already very high unit cost. Cargo yields consequently rose by 18.9% year on year, with the average rate reaching $2.75 per kilogramme, a monthly increase of 13.6%.

Despite cost pressure and the contraction in volumes, the global load factor remained stable at 47.9%, changing by just 0.1 percentage points compared with March 2025. This indicates that airlines were able to reduce the capacity offered broadly in proportion to the fall in demand, thereby preserving operating margins on the flights that were actually operated. Africa recorded the highest load factor increase, up 5.4 percentage points, while Europe confirmed the highest absolute level, at 59.9%.

IATA believes the broader macroeconomic backdrop remains generally favourable. According to its figures, global industrial production grew by 3.1% year on year in February 2026, marking the 38th consecutive month of expansion, while global goods trade increased by 8% over the same period. The global manufacturing PMI stood at 51.4 in March, above the 50-point expansion threshold, with the PMI for new export orders at 50.1. Willie Walsh, director general of IATA, said that "air cargo networks are providing the flexibility needed to support global supply chains as they adapt to geopolitical, tariff and operational pressures", adding that in the coming months the sector’s attention will remain focused on the evolution of fuel prices and supply.

Anna Maria Boidi