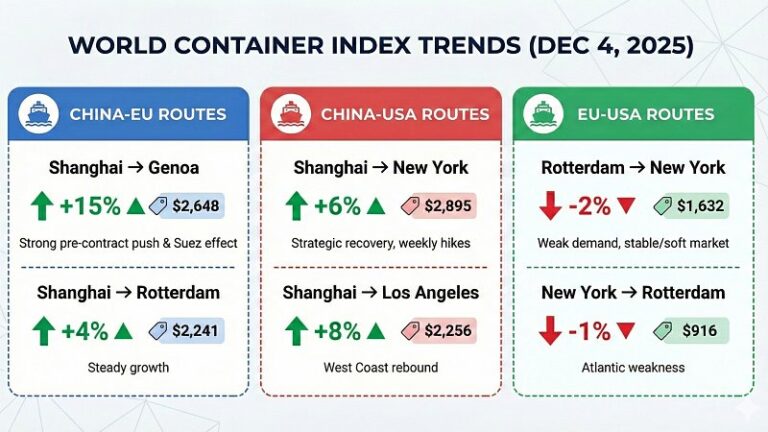

The weekly trend in average spot container freight rates recorded by the Drewry World Container Index as at 4 December 2025 registered a 7 per cent rise in the composite index, which aggregates all routes considered, climbing to 1,927 dollars for a 40-foot container. The year-on-year comparison remains negative: the current level is 45 per cent lower than in December 2024, underscoring the gap from the values reached during the recent expansionary cycle. After three weeks of contraction, which had pushed rates back to their lowest levels since January 2025, the market is showing signs of a reversal, particularly on the transpacific and Asia–Europe corridors. Atlantic routes remain static or in decline.

According to Drewry, the recovery is driven by both seasonal demand and a new pricing strategy adopted by some shipping lines. Carriers are replacing fortnightly freight rate increases with smaller rises applied weekly. The aim is to maintain steady upward pressure and prevent increases from dissipating quickly. This approach has helped fuel the current rebound, prompting Drewry to forecast stable rates in the following week.

On Asia–Europe routes the market has benefited for three weeks from the strengthening of fak rates applied by operators ahead of annual contract negotiations. Added to this is uncertainty over the full reopening of the Suez Canal. The corridor remains the natural link between Asia and the Mediterranean and a complete restoration of transits would bring additional capacity back into the system, exerting downward pressure on rates. The effect would still be gradual, as redeploying vessels along the east–west axis could generate congestion at ports.

Routes between China and the European Union show the most pronounced increases. The Shanghai–Genoa corridor reaches 2,648 dollars, a 15 per cent rise and an absolute increase of 348 dollars, around 323 euros. On an annual basis the decline remains steep at 52 per cent. The Shanghai–Rotterdam route rises by 4 per cent to 2,241 dollars, a 53 per cent drop compared with the same period last year. The rebound is more modest on the return leg, Rotterdam–Shanghai, which climbs by 2 per cent to 460 dollars, while the year-on-year comparison shows an 11 per cent fall.

On the transpacific front, the Shanghai–Los Angeles corridor records an 8 per cent increase, reaching 2,256 dollars, while the route to New York rises by 6 per cent to 2,895 dollars. The annual drop remains substantial, at 39 per cent and 44 per cent respectively. Moving against the trend, the return leg Los Angeles–Shanghai remains stable at 719 dollars, with no change from a year ago.

Transatlantic routes continue to show a weak trend. The New York–Rotterdam corridor falls by 1 per cent to 916 dollars, but remains the only link in the entire basket posting year-on-year growth, at plus 14 per cent. The Rotterdam–New York route drops by 2 per cent to 1,632 dollars, registering a 38 per cent decline from last year.

The overall picture confirms a market in an adjustment phase in which weekly increases are still not sufficient to offset the sharp reduction in rates seen over the past twelve months. The gradual reshaping of capacity along the main east–west trades, together with operational uncertainties linked to Suez, will continue to influence price dynamics in the coming weeks.