The second quarter of 2026 marked a turning point for air cargo: global spot freight rates surged by 30% year-on-year in April, reaching their highest level since October 2022. This is according to TransportIntelligence’s Air Freight Rate Tracker-Q2 2026 report, which attributes the acceleration not to organic demand growth, but to a structural supply-side shock triggered by the conflict that broke out in the Middle East at the end of February. The report states that headhaul routes averaged $3.7 per kilogramme in May 2026, up 35.85% year-on-year and 26.56% compared with the previous quarter, while backhaul routes stood at $2.9 per kilogramme, up 25.44% year-on-year and 17.90% quarter-on-quarter.

The most pronounced impact was seen on routes departing from Dubai, where rates tripled to $5.44 per kilogramme, a level with no recent precedent on the corridor. Jet fuel also weighed on price trends: during the peak of the conflict in March, the cost of jet fuel doubled, forcing carriers to apply heavy war-risk and fuel-price adjustment surcharges. In May 2026, the average global jet fuel index reached 470.4, up 275.8 points compared with the second quarter of 2025, according to TransportIntelligence. Brent crude was revised upwards to $96 a barrel, reflecting disruption in the Strait of Hormuz.

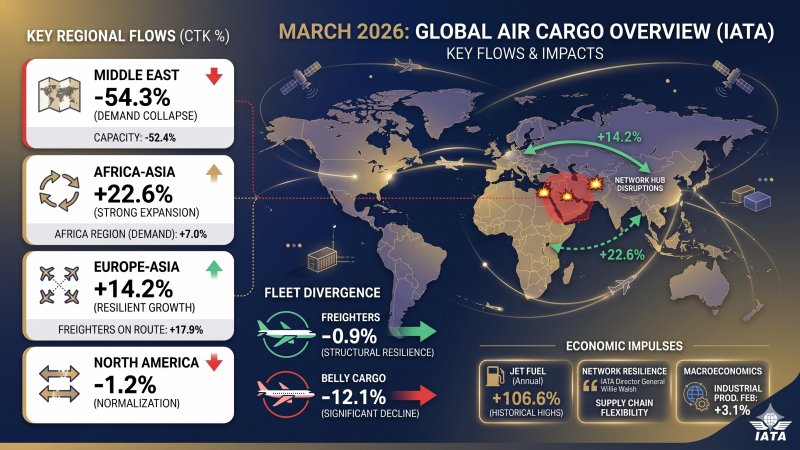

The trigger was the closure of Gulf airspace, which in just a few weeks removed a substantial share of transit capacity on routes between Asia and Europe. According to Iata data for March 2026, international cargo capacity measured in available cargo tonne-kilometres (ACTK) contracted by 6.8% year-on-year, a decline almost entirely attributable to the grounding or rerouting of flights that had crossed Middle Eastern hubs. On 1 March alone, more than 3,400 flights were cancelled at the seven main airports in the region.

In the months before the conflict, global demand had shown positive momentum, supported by Lunar New Year and buoyant e-commerce, with an increase of 11.2% in February. The picture reversed in March, when overall demand contracted by 4.8% year-on-year: Middle Eastern carriers suffered a collapse of 54.3%, while African and Asia-Pacific airlines showed relative resilience. The loss of bellyhold capacity on passenger flights, which forms the backbone of cargo supply, proved critical: the region’s nine main airports lost a combined total of about 620,000 tonnes of freight between March and April, equivalent to a 52% year-on-year decline.

The airport volume index for the first quarter of 2026 stood at 104.5 globally, down 1.6 points year-on-year and 16.4 points lower than in the fourth quarter of 2025, reflecting both seasonal effects and the post-shock downturn. Against this backdrop, Europe was the only macro-region to record year-on-year growth, with a 5.5-point increase that took the index to 117.1. North America recorded the sharpest contraction, losing 12.8 points and bringing the index down to 94.0.

The first signs of stabilisation appeared in May, alongside the announcement of a ceasefire. Airlines such as Emirates and Qatar Airways began gradually restoring operations. However, additional freighter capacity remains limited by delays in new aircraft deliveries and the ageing of the global fleet, leaving the market structurally dependent on the full recovery of passenger routes in the Middle East. Airlines remain cautious, aware that geopolitical risks have not yet subsided.

Operator sentiment reflects this situation. According to the report, 70.5% of respondents globally expect air freight rates to continue rising in the three months following the survey. The figure rises to 73.1% on the Asia-North America West Coast route and to 73.3% on the Asia-North West Europe route. TransportIntelligence’s outlook matrix positions supply chain disruption and fuel costs as consistently upward drivers throughout the second and third quarters of 2026. On the regulatory front, the report identifies a further source of uncertainty for the months ahead: the removal of “de minimis” exemptions in the European Union by 2027 could lead to a short-term fall in cross-border e-commerce volumes, further altering the balance on the demand side and making the sector’s recovery outlook even more uncertain.

Anna Maria Boidi