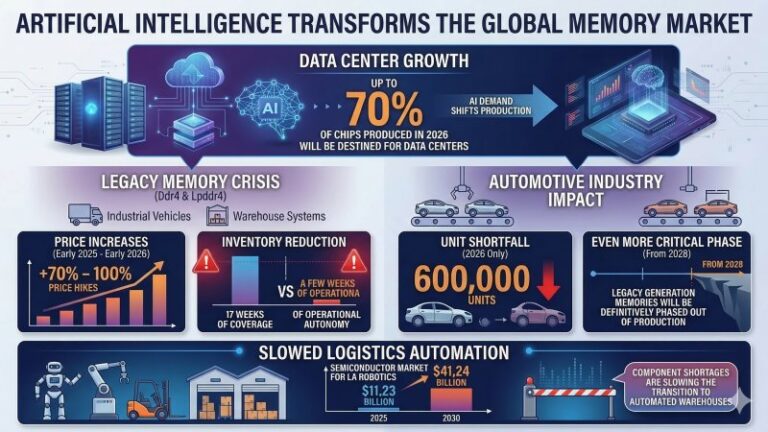

- Artificial intelligence has reshaped the global memory market, with up to 70% of chips produced in 2026 destined for data centres. Legacy memories such as DDR4 and LPDDR4, which are essential for industrial vehicles and warehouse systems, saw price increases of between 70% and 100% between early 2025 and early 2026, while inventories have fallen from 17 weeks of coverage to just a few weeks of operational autonomy.

- The crisis is spreading to vehicle production, with the automotive industry estimating that around 600,000 units will not be built in 2026 alone. The sector is bracing for an even more critical phase from 2028, when older-generation memory will be definitively phased out of production.

- Logistics automation is facing similar challenges. The semiconductor market for robotics is valued at $11.23 billion in 2025 and is expected to reach $41.24 billion by 2030, but component shortages are slowing the transition to automated warehouses.

The crisis affecting European logistics in 2025–2026 bears little resemblance to previous disruptions. It is not a repeat of the pandemic shock of 2020–2022, which stemmed from temporary operational interruptions and maritime bottlenecks. This time the cause is structural, deliberate and, at least in the medium term, irreversible. The three giants controlling more than 80% of global DRAM memory production — Samsung Electronics, SK Hynix and Micron Technology — have chosen to shift their production lines decisively towards high-bandwidth memory (HBM), the component that powers the graphics processing units used to train artificial intelligence models. This decision is driven by clear financial logic: margins from contracts with major data centre operators are significantly higher than those historically offered by the automotive industry or industrial equipment manufacturers.

The consequences of this reallocation are spreading across the backbone of logistics, from vehicle manufacturers to automated warehouse operators and small haulage firms. Producing a single gigabyte of HBM requires three to four times the silicon wafer capacity of standard DRAM, disproportionately absorbing production capacity. Projections indicate that up to 70% of high-end memory chips produced globally in 2026 will be allocated exclusively to AI data centres. This represents an unprecedented share in the history of electronics, leaving traditional industrial sectors competing for limited supply.

The most immediate sign of this imbalance is the sharp decline in inventories of conventional memory chips. Global DRAM stock levels at suppliers have fallen from 17 weeks of coverage at the end of 2024 to just a few weeks of operational capacity during 2025. The impact on prices has been immediate and severe. Between early 2025 and early 2026, legacy chips such as DDR4 and LPDDR4 rose in price by between 70% and 100%, with lead times stretching unpredictably and no normalisation expected before 2027 or 2028. Supply growth for DRAM and NAND in 2026 is projected at 16% and 17% year on year respectively, well below the historical averages needed to sustain the pace of industrial digitalisation.

The scale of the impact on automotive can be understood by noting that around 95% of chips currently installed in road vehicles are based on mature or legacy nodes — precisely those that foundries are progressively discontinuing to free up capacity for advanced AI chips. In modern industrial vehicles, the increasing adoption of driver assistance systems (ADAS), digital dashboards, V2X connectivity and advanced telematics has almost multiplied memory requirements tenfold per vehicle. In high-end freight transport models, the value of DRAM modules alone now exceeds $100 (around €92) per unit, compared with less than $10 in earlier-generation base vehicles.

Analysts identify two distinct phases in the progression of this crisis. The first, covering 2026–2027, is characterised by technically available supply at prohibitive prices. Tier 1 suppliers are expected to build safety stocks, triggering a “panic buying” mechanism that artificially inflates supply contracts. The second phase, beginning in 2028, will mark the onset of a true structural shortage, when supplies of legacy chips may decline rapidly and permanently, regardless of buyers’ willingness to pay. This outlook is pushing vehicle manufacturers to complete the redesign of onboard electronic systems, migrating to architectures based on LPDDR5 memory. This is not limited to display upgrades but extends to the homologation of ADAS under functional safety standards such as ISO 26262, requiring lengthy validation cycles including thermal and electromagnetic stress testing.

The crisis is also affecting fixed logistics infrastructure. Modern intralogistics systems — sensor networks, autonomous mobile robots and automated storage and retrieval systems — depend on the same legacy chips that the automotive industry is struggling to source. The semiconductor market for robotic systems is valued at $11.23 billion in 2025 and is projected to reach $41.24 billion by 2030, with a compound annual growth rate of 29.7%. However, component shortages are acting as a brake on this trajectory.

In response, the more structured vehicle manufacturers and logistics operators are moving away from just-in-time models in favour of regional sourcing strategies, with direct multi-year contracts signed with chip foundries, bypassing intermediaries. The goal is not to eliminate price increases — impossible without the bargaining power of major technology players — but to secure minimum wafer allocations and prevent prolonged shutdowns of assembly lines. This situation could accelerate the adoption of digital twins: high-fidelity simulations of entire warehouse systems used to identify precisely which hardware investment — whether a robotic arm, an additional conveyor or a software upgrade — delivers the highest return on capital tied up in scarce and costly chips.

Pietro Rossoni