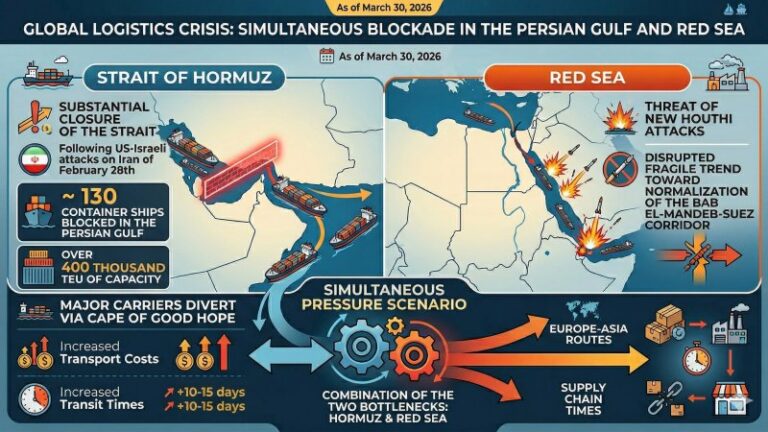

- As of 30 March 2026, around 130 container ships — representing more than 400,000 TEU of capacity — are stranded in the Persian Gulf following the effective closure of the Strait of Hormuz after the US-Israel attacks on Iran on 28 February. Major carriers have rerouted services via the Cape of Good Hope, increasing both costs and transit times.

- In the Red Sea, the threat of new Houthi attacks has interrupted the fragile trend towards normalisation along the Bab el-Mandeb–Suez corridor. The combination of the two bottlenecks — Hormuz and the Red Sea — creates a scenario of simultaneous pressure on both access routes to Gulf and Asian markets, with repercussions for Europe–Asia routes and supply chain transit times.

- The structural context remains one of overcapacity: according to Bimco, container transport demand is expected to fall by around 5% in 2026, while fleet capacity continues to grow. The result is a market with generally depressed freight rates but high volatility, with war risk surcharges reaching up to $4,000 per container on some routes.

Global container shipping is facing, as of 30 March 2026, a two-front geopolitical crisis that is simultaneously constraining the two most strategic maritime corridors for flows between Asia, Europe and the Middle East: the Strait of Hormuz and the Red Sea. One month after the attacks carried out by the United States and Israel against Iran — which began on 28 February — the situation has yet to stabilise, and the outlook for the coming months remains uncertain.

In the Persian Gulf, according to Bimco estimates, around 130 container ships remain stranded, removing more than 400,000 TEU of capacity from the market. This represents around 1.5% of total global container fleet capacity, a share which — based on AIS data analysis — corresponds to roughly 3% of global volumes no longer able to move and around 5% of global vessel demand. Expanding the scope to all types of commercial vessels — tankers, bulk carriers, general cargo ships as well as container ships — between 20 and 22 March up to 1,900 units were either blocked or significantly delayed in the Hormuz–Gulf area, according to data reported by Anadolu Agency.

The de facto closure of the Strait originated from actions by Iranian authorities, which initially blocked the passage and threatened intervention against transiting vessels. At the same time, many insurers suspended war risk coverage for the area, making commercial transit unviable even for operators willing to face the physical risk. Major carriers have therefore diverted their services via the Cape of Good Hope, resulting in longer voyage times and higher operating costs linked to increased fuel consumption and the management of extended rotations.

Between 25 and 27 March, the first signs of selective easing emerged: Chinese media sources reported that at least two Cosco container ships had begun transiting the Strait to return to China, and that Iran had agreed to allow a limited number of Pakistani-flagged vessels to pass. These remain negotiated and partial reopenings rather than a full normalisation of the corridor. Bimco stresses that uncertainty will remain high even if transits resume on a broader scale in the coming weeks, prompting carriers and insurers to maintain risk premiums and alternative routings.

According to an estimate reported by Reuters, many services calling at Gulf ports also served Pakistan and India: it is estimated that up to around 10% of the global fleet is affected in some way, with vessels stranded, rerouted or forced to reschedule rotations. Supply chains reliant on Gulf ports are adopting alternative solutions — external hubs such as Salalah and Jeddah, land corridors and transhipment — but with increased costs and transit times. Some vessels no longer able to serve Gulf ports regularly are being idled or used as contingency capacity, rather than redeployed on other routes, to avoid further downward pressure on already depressed freight rates.

The disruption is adding significant costs for operators: war risk premiums, insurance surcharges, higher fuel consumption due to diversions, and the management of immobilised ships and crews. Some shipping lines and freight forwarders have introduced emergency war risk surcharges, in some cases reaching $4,000 per container, alongside projected bunker adjustment factor (BAF) increases of between 20% and 40% over the next 30 to 90 days on affected routes.

The Hormuz crisis overlaps with renewed tensions in the Red Sea, where the Houthis announced between late February and early March the resumption of missile and drone attacks against commercial vessels in the Gulf of Aden, in response to the US-Israel strikes on Iran. On 28 March, governments and analysts raised the alarm following a Houthi missile launch towards Israel, interpreted as a signal of a likely extension of attacks to maritime traffic in the Red Sea. The mere public declaration of the campaign’s resumption, combined with missile launches, has been enough to raise alert levels among naval forces and shipping companies, even in the absence — as of 30 March — of a new wave of confirmed large-scale sinkings or hijackings.

The experience of 2023–2025 weighs heavily on operators’ assessments: during that period, more than 100 merchant vessels were attacked or targeted by the Houthis, four ships were sunk, one seized and at least eight seafarers killed, before a truce concluded in 2025. This operational memory is driving widespread caution in resuming transits via the Red Sea–Suez corridor. As early as 1–2 March 2026, Maersk and other major lines stopped treating the Red Sea–Suez route as a corridor on a path to normalisation, reinforcing diversions via the Cape.

The combination of the two scenarios — an almost closed Hormuz and renewed Houthi threats in the Red Sea — is being interpreted by analysts as a dual bottleneck scenario: two key passages under pressure simultaneously, with potentially systemic impacts on global container flows, particularly on Asia–Europe and Asia–Mediterranean routes.

However, the underlying backdrop remains one of structural fleet overcapacity. According to Bimco forecasts, container transport demand is expected to decline by around 5% in 2026, while fleet growth continues to outpace demand, weakening the supply-demand balance over the 2026–2027 period. The geopolitical crisis introduces significant volatility into this context: a non-negligible share of capacity is physically blocked or rendered inefficient, yet the structural trend remains one of generally depressed freight rates, with upward spikes linked to localised congestion and tactical capacity management by carriers. For freight forwarders, the market remains broadly favourable in the medium term, but with potential short-term spikes driven by geopolitical developments and the management of rerouting.

The crisis also has a humanitarian dimension: several sources estimate that tens of thousands of seafarers are stranded in the Persian Gulf, with growing logistical and psychological challenges on board. Restrictions on port calls, crew changes and the evacuation of people and cargo are further complicating operations for companies active in the region.

M.L.