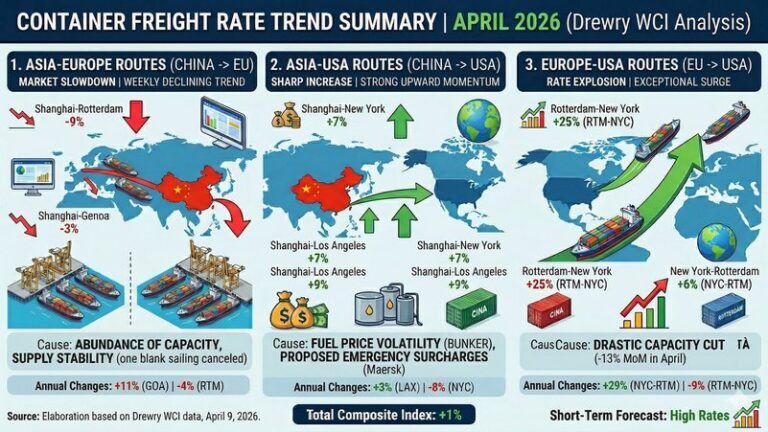

Drewry’s average spot container freight rates, published on 9 April 2026, show a mixed weekly trend. The composite World Container Index rose slightly by 1% to reach 2,309 dollars per 40-foot container, but this average across all routes masks diverging dynamics on the main trade lanes. Geopolitical tensions linked to the Strait of Hormuz, volatility in fuel costs and carriers’ capacity management strategies are all shaping flows between Asia, Europe and the United States.

The key driver this week is fuel costs, influenced by uncertainty in the Strait of Hormuz, a chokepoint through which around 20% of global oil supply passes. Despite a temporary ceasefire, operating conditions remain unstable and shipping companies are prioritising the repositioning of vessels already in the Persian Gulf. In this context, Maersk has asked US authorities for approval to introduce an immediate emergency fuel surcharge of 200 dollars per TEU on headhaul routes and 100 dollars per TEU on backhaul routes, signalling a sharp increase in operating costs.

These cost pressures are clearly reflected on routes to North America. The transatlantic corridor recorded the strongest variation: rates between Rotterdam and New York rose by 25% in a week to 1,968 dollars, while the reverse route increased by 6% to 1,063 dollars. This trend is not driven solely by higher fuel costs, but also by reduced available capacity. Ocean capacity on this route is down by 13% for April, tightening supply and supporting prices.

The transpacific market is also trending upwards. Shipments from China to the US West Coast rose by 9% to 2,910 dollars, while rates to the East Coast increased by 7% to 3,671 dollars. In this case, alongside energy costs, carriers appear to be pursuing a strategy of rapidly passing cost increases on to shippers, also in anticipation of new surcharges.

By contrast, Asia–Europe routes are moving in the opposite direction. The Shanghai–Rotterdam route fell by 9% to 2,308 dollars, also showing a year-on-year decline of 4%. The Shanghai–Genoa route dropped by 3% to 3,420 dollars. According to Drewry’s Container Capacity Insight, downward pressure on this corridor is driven by abundant capacity: only one sailing cancellation is expected in the following week, indicating capacity remains largely unchanged and above demand. In these conditions, carriers are lowering rates to maintain high load factors.

Drewry’s outlook suggests that pressure on westbound freight rates is unlikely to ease in the short term. A normalisation of energy flows through Hormuz will take time, keeping fuel cost uncertainty elevated. In this environment, shipping lines are expected to continue supporting rate levels, with potential further increases on the most exposed routes.