- Between 28 February and 2 March 2026, the military crisis in the Middle East led to the closure or restriction of numerous flight information regions and resulted in more than 3,400 cancellations, with over 2,000 flights grounded on 1 March alone. Dubai, Doha and Abu Dhabi have been operationally neutralised, blocking large cargo volumes as well.

- Before the crisis, the air cargo market had been showing solid momentum: global demand was up 5.6% year on year in January 2026 and capacity had increased by 5%, with the dynamic load factor at 57%. Average global spot rates stood at 2.56 US dollars per kg, while jet fuel prices were down 6.5% year on year. The shock has abruptly disrupted this balance.

- The loss of bellyhold capacity and the closure of Gulf hubs have triggered an 18% drop in global capacity within a week and a 26% collapse on the Asia–Middle East–Europe corridor over the first weekend. Reroutings, payload penalties and the maritime crisis are amplifying cost increases.

As of 2 March 2026, the global air freight infrastructure has entered an operational fracture phase with few precedents since the Covid-19 pandemic. The sequence has been rapid: the joint US–Israeli military operation “Epic Fury” against Iran, launched on 28 February 2026, prompted Tehran’s retaliation, “True Promise 4”, opening a theatre that has not remained confined to Israel. The response has also targeted US installations in allied countries and has extended to the United Arab Emirates, Qatar, Bahrain, Kuwait, Oman, Jordan and Iraq, with immediate consequences for civil aviation: the full or partial closure of airspace and the disconnection of the main east–west axis between Asia Pacific and Europe, as well as routes to the Americas.

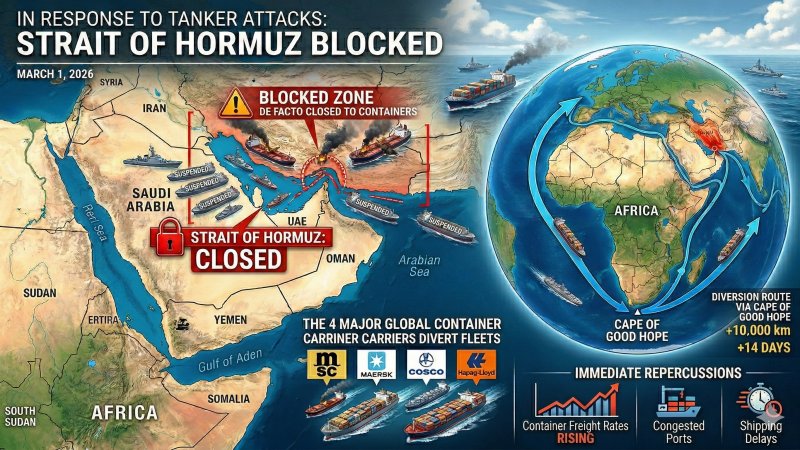

In the first 48 hours, the shock took on a systemic character as it affected both air and sea. The source describes the de facto closure of the Strait of Hormuz by the Islamic Revolutionary Guard Corps and a renewed suspension of Red Sea transits by major ocean carriers, producing a combined effect that has not merely diverted routes but paralysed nodes, services and flows. For logistics operators, the difference compared with many previous crises lies in the simultaneity of the blockages: it is not simply a matter of avoiding one area, but of losing within hours a network of gateways underpinning intercontinental transit architecture, particularly for air cargo and intermodal models.

Before the escalation, the air cargo market had opened 2026 with robust dynamics. In January 2026, global demand measured in cargo tonne kilometres rose by 5.6% year on year, while demand measured in chargeable weight increased by 7%, the highest figure in the past twelve months. Global capacity grew by 5%, pushing the dynamic load factor to 57%, one percentage point above the previous year. On pricing, average global spot rates stood at 2.56 US dollars per kilogramme, down 1% year on year, signalling stabilisation after post-pandemic volatility. Fuel prices in the same month were down 6.5% year on year, against a backdrop of a slight 0.8% decline in global cargo yields. It is this already delicate equilibrium, marked by regional divergences and mixed signals from Chinese e-commerce, that the crisis has disrupted.

What has turned the military event into a global emergency for commercial aviation is the fragmentation of airspace. Between 28 February and 2 March 2026, a progressive “seal” was imposed on vast areas of airspace through Notam bulletins, aimed at reducing the risk of accidental shootdowns of civilian aircraft in an environment saturated with air defences, ballistic missiles and drones. Alongside kinetic threats, electronic warfare has emerged as a risk factor, potentially disrupting communications and satellite navigation and increasing operational uncertainty for commercial flights in transit. On 1 March alone, more than 2,000 flights to and from the Middle East were cancelled, around 50% of the region’s scheduled traffic for the day. Between 28 February and 1 March, cancellations exceeded 3,400, with immediate repercussions for passengers and cargo alike.

The operational picture shows full closures or severe restrictions across numerous flight information regions. Tehran (OIIX) is fully closed, with capacity cut by 100% and overflights along the optimal Asia–Europe corridor halted. Baghdad (ORBB) is also fully closed, with an estimated 84% capacity reduction and mandatory reroutings. Tel Aviv (LLLL) is fully closed with no authorised priority traffic and a 78% capacity cut, with both passenger and cargo commercial flights suspended. Doha (OTDF) is fully closed and suspended, while the UAE area (OMAE) is partially closed with dynamic restrictions and a severe capacity reduction. Additional airspace has been closed or restricted in Bahrain, Kuwait, Jordan, Lebanon, Oman and Saudi Arabia, creating a widespread disconnection of the Arabian Peninsula and the Levant from intercontinental networks.

The heaviest blow for logistics has come as the crisis shifted from routes to infrastructure. Dubai International (DXB), Hamad International in Doha (DOH) and Zayed International in Abu Dhabi (AUH) have been physically impacted and operationally neutralised, severing one of the world’s busiest east–west corridors. In Dubai, minor structural damage has been reported at Terminal 3 following falling debris linked to an alleged drone or intercepted missile attack, with seven people injured among staff and civilians and operations suspended indefinitely. For Emirates and its Emirates SkyCargo division, the closure puts around 10,000 tonnes of daily cargo capacity at risk. In Abu Dhabi, a drone attack caused one fatality and seven injuries, leading to flight suspensions and the grounding of Etihad operations. In Kuwait, Terminal 1 sustained limited damage with minor injuries, while in Bahrain material damage without casualties has nonetheless paralysed Gulf Air flights. In Qatar, the airspace closure has grounded Qatar Airways and removed approximately 12,000 tonnes of daily cargo capacity.

Operationally, this has meant aircraft and crew dispersion and the need for repositioning outside risk areas. It is a genuine “logistical nightmare” linked to global rostering and asset redeployment. For freight operators, however, the most critical variable is bellyhold capacity, as a significant share of global air cargo moves on passenger aircraft. The source estimates that between 30% and 40% of air freight traded between Europe and Asia typically transits through Middle Eastern hubs, relying on widebody belly cargo. When the passenger fleets of Emirates, Qatar Airways and Etihad are grounded and several international carriers cancel flights to or through the region, that capacity evaporates abruptly.

The scale of the collapse is measurable. Rotate estimates an 18% drop in global air freight capacity within a single week. Aevean reports that on the Asia–Middle East–Europe corridor, capacity in ACTK terms fell by 26% over the first weekend of the crisis, between 28 February and 2 March. Structural vulnerability is also evident in fourth-quarter 2025 data: around 50% of capacity between China, including Hong Kong, and Europe is operated via direct flights, while the remaining 50% depends on intermediate stops in the Middle East or Central Asia. With Gulf hubs neutralised, that “indirect” half becomes extremely difficult to recover in the short term.

The industry’s immediate response has been a forced shift towards long-haul direct flights and greater deployment of dedicated freighters. Overall, direct cargo capacity between Asia and Europe has increased by 13–14%, with direct freighter capacity up 34%, while capacity on flights stopping in the Middle East has collapsed by 75%. This urgent rebalancing highlights technical and economic constraints. Many freighters require intermediate refuelling stops and, with Dubai, Doha and Abu Dhabi unavailable, secondary hubs further north in Central Asia and the Caucasus have come into play. Almaty and Tbilisi have emerged as relief valves for the Eurasian network, while some Asia–North America flows are being rerouted over the Pacific, bypassing the Middle East entirely.

From here, operational developments merge with strategic considerations, as rerouting is not merely a matter of time. Average transit times have lengthened by four to six hours, a physical constraint that in air logistics quickly translates into reduced effective capacity through payload penalties. Longer routes require more fuel, with consumption per leg estimated to rise by up to 30%. Given maximum take-off weight limits, more fuel means less cargo. As a result, even where flights remain operational, the cargo density per flight declines. To mitigate the impact, some carriers have introduced technical refuelling stops, adding delays, airport charges and crew management complexity.

The energy shock is compounding the problem just as fuel consumption rises. Brent futures have climbed by up to 13%, briefly exceeding 82 US dollars per barrel before stabilising around 78 dollars. The impact on jet fuel has been even sharper: around 20% of global aviation fuel volumes transit through the Strait of Hormuz, and with the blockade, short-term delivery premiums in Europe have doubled within hours. Attacks on Saudi energy infrastructure, including the 550,000 barrel-per-day Ras Tanura refinery, have further disrupted output. In this context, higher costs and lost payload converge into a margin erosion risk for carriers already operating on thin profitability.

On freight rates, the typical capacity-crisis pattern is emerging: initial inertia in long-term contracts and immediate volatility in the spot market, where scarce belly space and rising operating costs fuel a rapid upward spiral. On some Asia–Europe routes, last-minute spot rates have doubled or tripled within 24 hours. For freight forwarders, the challenge is not only cost but availability: major carriers are limiting new bookings and backlogs are building, with a cautious estimate of seven to ten working days to clear volumes stranded at various Asian gateways, even assuming a full and immediate reopening of Middle Eastern airspace.

Carriers’ operational decisions confirm the emergency logic. Emirates has suspended operations to and from Dubai until at least 15:00 on 3 March, with only a slow and partial restart for passengers holding prior bookings. Qatar Airways has suspended all flights to and from Doha. Etihad has halted departures from Abu Dhabi for security reasons. Lufthansa has suspended several destinations until 8 March and has declared a cargo embargo on Dubai, Abu Dhabi and Riyadh from 1 to 8 March for perishables, live animals, valuables and human remains. Cathay Pacific has cancelled passenger and freighter services to and from Dubai and the Middle East until 5 March. FedEx has suspended pick-up, delivery and flight services in an extensive list of countries, invoking force majeure. Air India has suspended direct Middle East flights and, to maintain links with Europe and North America, is routing via technical stops in Europe, with Rome Fiumicino among the examples. Air Canada has cancelled routes to the region and extended rebooking policies until 15 March for several destinations.

Lufthansa Cargo’s selective embargo is strategically significant, highlighting the point at which the logistics chain can no longer guarantee handling standards. The excluded categories, such as perishables, temperature-controlled goods, live animals and valuables, are precisely those for which air cargo is often irreplaceable. If an airport cannot ensure timing certainty and cold chain integrity, the carrier removes the risk by refusing shipments at origin. For warehouse and transport operators, the focus therefore shifts from freight rates alone to the availability of suitable infrastructure and manageable slots, with direct implications for value-added services ranging from temperature control to security.

As real-time crisis management gives way to strategic assessment, another multiplier emerges: the maritime disruption and the effective “end” of the sea–air model. The de facto closure of the Strait of Hormuz and the abandonment of Red Sea and Suez Canal corridors are forcing widespread rerouting of container ships around the Cape of Good Hope. This absorbs around 2.5 million TEU of capacity simply to cover longer transit times and extends Asia–Europe voyages by 10 to 14 days. Economically, significant war-related surcharges have been introduced, including a “War Risk Surcharge” announced by Hapag-Lloyd of 1,500 US dollars per TEU and 3,500 US dollars per reefer and special container to or via the Persian Gulf, and an “Emergency Surcharge” indicated by CMA CGM of 4,000 US dollars per 40-foot container for the region. For cargo owners, the result is twofold: extended contractual delivery times and additional costs that erode margins and increase pressure on final prices.

The breaking point for intermodality is Jebel Ali and, more broadly, the sea–air logistics bridge. Many companies shipped from Asia to ports on the Arabian Peninsula, cleared customs and transferred cargo by road to nearby airports for onward flights to Europe or North America, halving transit times at an intermediate cost. With Hormuz sealed and the temporary suspension of operations at DP World’s Jebel Ali terminal, that bridge has collapsed. Demand is shifting from sea to air precisely as the air market loses capacity and hubs. This is pushing unplanned volumes onto South-East Asian and Chinese airports and adding upward pressure on rates, while repeated force majeure claims on contracts can be expected.

In this reconfiguration, competitive asymmetries linked to existing geopolitical constraints are also emerging. Chinese and other Asian carriers not subject to Russian airspace restrictions retain an advantage by using the Siberian corridor to reach Europe. Western carriers, barred from Russian skies and now unable to use the southern axis crossing Turkey, Iraq and Iran towards the Gulf, are forced into longer diversions that call operational sustainability into question. India and South Asia are particularly hard hit: given their historical reliance on Gulf mega-hubs, capacity to and from the subcontinent has fallen by more than 60%, and alternative hubs such as Muscat are rapidly saturating.

Regulatory management is proceeding under the principle of flight safety. The European Union Aviation Safety Agency has issued Conflict Zone Information Bulletin CZIB 2026-03 dated 28 February 2026, designating all flight levels as high risk for the flight information regions of Bahrain, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Oman, Qatar, the United Arab Emirates and Saudi Arabia. In parallel, it has reiterated the obligation for airlines to conduct their own risk assessments, a practice reinforced after the downing of Ukraine International Airlines flight 752 over Tehran in 2020, cited as a precedent of misidentification under operational stress.

M.L.