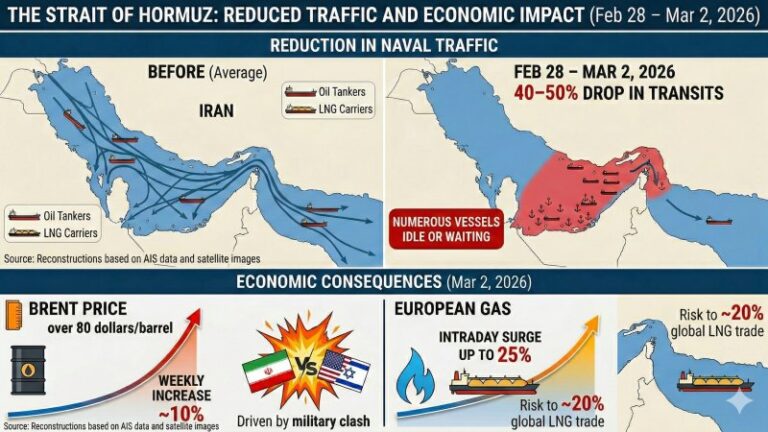

- Traffic of oil tankers and LNG carriers in the Strait of Hormuz was sharply reduced between 28 February and 2 March 2026, with transits down by 40–50% and numerous vessels stationary or waiting in the Persian Gulf, according to reconstructions based on AIS data and satellite imagery.

- The military confrontation between Iran, the United States and Israel pushed Brent above 80 dollars a barrel on the morning of 2 March 2026, with weekly gains of around 10%, while European gas recorded an intraday jump of up to 25% amid risks to roughly 20% of the global LNG trade that passes through Hormuz.

- Marine insurers have suspended or restricted cover in the area and raised war risk premiums to levels comparable with those seen in the Black Sea after Russia’s invasion of Ukraine. Some units of the so-called shadow fleet continue to operate on high-risk routes, using non-traditional insurance arrangements.

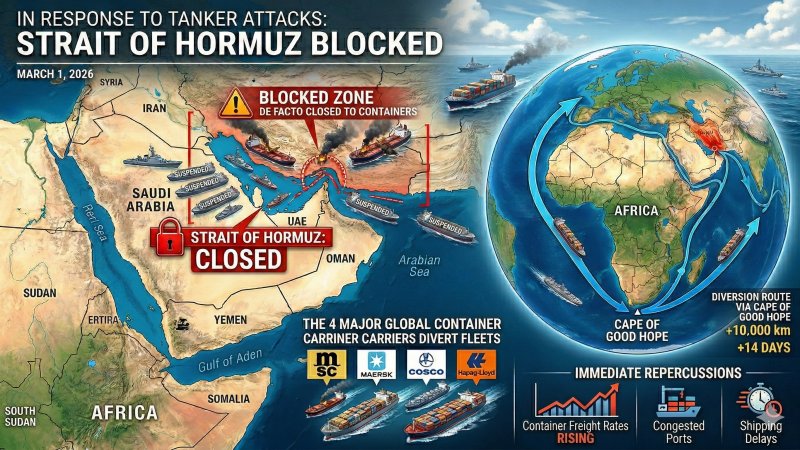

At 11:00 on 2 March 2026, tanker and LNG carrier traffic in the Strait of Hormuz was heavily disrupted following the military confrontation between Iran, the United States and Israel. Between 27 and 28 February, Iran declared the closure of the strait after a series of attacks, with transits estimated to be down by between 40% and 50% compared with previous levels. The main crude oil and liquefied natural gas export routes of Saudi Arabia, the United Arab Emirates, Iraq, Qatar and Iran are therefore exposed to heightened operational risk.

Vessel tracking shows tankers and gas carriers either stationary or moving at minimum speed in the Persian Gulf, with millions of barrels on board awaiting instructions. Hundreds of vessels are effectively idle or at anchor near the strait, while some captains have reversed course before entering the transit corridor. Iran’s Islamic Revolutionary Guard Corps is reported to have issued radio warnings to merchant vessels, increasing the perception of insecurity among shipowners and insurers.

The tension has been immediately reflected in energy markets. Brent was trading above 80 dollars a barrel on the morning of 2 March, up around 10% compared with late February levels of 71–73 dollars. Technical analysis points to a break above resistance around 74 dollars, with the upward trend supported by a geopolitical risk premium. Traders are pricing in not only the disruptions already observed but also the possibility of a prolonged blockage of the world’s main energy chokepoint.

On the gas side, international benchmarks stood at around 3 dollars per MMBtu on 2 March, up 4–5% on a daily basis. In Europe, the TTF future posted an intraday jump of up to 25%, the sharpest since 2023, on fears of disruptions to LNG flows from Qatar, which account for around 20% of global seaborne liquefied natural gas trade. Despite the spike, prices remain about 27% lower year on year, indicating that the shock is concentrated in the very short term.

Further pressure is coming from the insurance market. Following attacks on tankers in the area between Hormuz and the Gulf of Oman, several marine insurers have suspended or restricted cover for vessels bound for the strait and increased war risk premiums. According to industry sources, these levels are comparable to the peaks seen in the Black Sea after the start of the Russia–Ukraine war in 2022. Higher insurance costs are directly affecting freight rates and the overall cost of the energy logistics chain.

In this context, differences are emerging between operators. Some segments of the so-called shadow fleet, particularly gas carriers and tankers linked to Russian energy exports, continue to use high-risk routes such as the Red Sea despite tensions, partly for economic reasons and due to the limited availability of operational alternatives. Companies with less exposure to Western regulations or with insurance cover outside traditional markets appear more willing to operate in critical areas, albeit with more fragile safety profiles.

From a logistics perspective, the reduction in transits at Hormuz adds to tensions in the Red Sea and at Bab el-Mandeb, prompting several carriers to reconsider transits via Suez or to evaluate longer routes around the Cape of Good Hope. Longer voyage times reduce spot market capacity and help to support freight rates, with knock-on effects on crude and LNG procurement costs for Europe and Asia.

P.R.