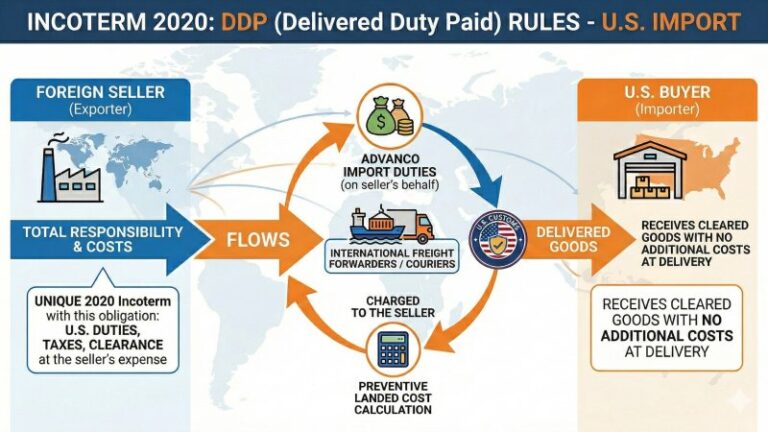

- Under Ddp (Delivered Duty Paid), it is the foreign seller, not the buyer, who must bear duties, taxes and customs clearance costs when goods enter the United States. It is the only Incoterm 2020 that assigns this obligation to the exporter.

- In practice, the seller does not pay US Customs directly but relies on freight forwarders or international couriers to advance import duties on its behalf, which are then recharged based on a prior calculation of the landed cost.

- Adopting Ddp for shipments to the US entails significant risks for the exporter: customs classification errors, underestimation of duties, potential anti-dumping or countervailing duties, and the need to manage the role of importer of record within the framework of US federal regulations.

In international trade with the United States, the question of who pays import duties largely depends on the Incoterm chosen by the parties in the sales contract. The answer is not straightforward: only in the case of Ddp — short for Delivered Duty Paid — does the obligation fall entirely on the foreign seller, except where specific agreements signed between the parties provide otherwise. Under all other commonly used contractual terms, from Exw to Fob and Cip, import duties and customs formalities are borne by the buyer.

Ddp is defined by the Incoterms 2020 of the International Chamber of Commerce as the term that assigns the maximum level of obligations to the seller: it must arrange transport, bear all costs, complete both export and import formalities and pay duties and taxes in the country of destination. The goods are delivered to the buyer cleared for import at the agreed place, with no additional payment due from the recipient at the time of delivery.

In practical terms, a seller operating under Ddp to the US assumes a series of clearly defined cost items. The main component is customs duties, calculated on the basis of the goods’ Hs code, declared origin and customs value. These are accompanied by customs clearance charges, customs broker fees, the Merchandise Processing Fee and other administrative charges required by US Customs, namely U.S. Customs and Border Protection (Cbp). In many cases, the Ddp price also includes insurance and ancillary handling charges, so that the US buyer faces no additional costs.

One frequently misunderstood aspect concerns the operational mechanics of payment. In many cases, the foreign seller does not pay duties directly to Cbp but instead uses international freight forwarders or couriers that advance the import duties on its behalf. These intermediaries then recharge the amounts to the seller, usually on the basis of a landed cost estimate agreed before shipment. Many couriers and e-commerce platforms allow duties and taxes to be calculated and collected at checkout, enabling the exporter to offer Ddp delivery with a transparent final price and no surprises for the recipient.

From a legal and customs perspective, it should be noted that the US buyer, or an importer of record designated by it, often remains the party formally appearing in declarations to Cbp, even when the economic cost of the duties is entirely borne by the seller. This split between the legal subject and the economic subject is one of the operational peculiarities of Ddp to the US and requires careful management of compliance responsibilities.

The use of Ddp has intensified in recent years, particularly in shipments to final consumers and in cross-border e-commerce. The growth of this model has been supported by the development of dedicated logistics services that make it possible to pre-invoice duties to the exporter, eliminating the risk of failed delivery or refusal of goods by the recipient due to unexpected customs charges. There has been increasing recourse to Ddp in e-commerce shipments to the US also in response to changes to the de minimis threshold for certain origins.

The US tariff environment has become more complex in recent years. The introduction and adjustment of additional duties — such as those under Section 232 on steel and aluminium, Section 301 on certain products of Chinese origin, and specific measures affecting certain product categories — have made it more difficult for sellers to estimate accurately the total cost of customs clearance when setting a Ddp price. From 2025, the general elimination of the de minimis exemption above 1 dollar in value effectively makes every shipment subject to duty or tax, further increasing the importance of correctly allocating costs in Ddp transactions.

The risks for sellers choosing Ddp to the US are numerous and should not be underestimated. An error in tariff classification through the use of an incorrect Hs code can lead to customs reassessments and penalties. Underestimating applicable duties — particularly where anti-dumping measures, countervailing duties or extraordinary tariffs apply — can significantly erode sales margins. There is also the risk of shipments being blocked for non-compliance with specific regulations, such as the Uyghur Forced Labor Prevention Act, which imposes stringent documentary requirements for certain categories of products of Chinese origin.

To manage Ddp shipments to the US properly, sellers must also assess whether fiscal registration in the country of destination is required, as assuming responsibility for import taxes may trigger broader federal and state tax obligations. Several experts recommend using Ddp for US shipments only where the exporter has reliable partners on US territory, adequate knowledge of US customs regulations and real-time landed cost calculation systems. In the absence of these conditions, it may be preferable to use terms such as Dap (Delivered at Place), leaving the buyer responsible for paying duties at customs, albeit at the cost of greater complexity for the purchaser.

Anna Maria Boidi